Table of Contents

PostCapitalism: A Guide to Our Future by Paul Mason, 2015, London: Allen Lane

Introduction

In short, the argument of this book is

that capitalism is a complex, adaptive system which has reached the limits of its capacity to adapt.1)

According to the OECD, growth in the developed world will be 'weak' for the next fifty years. By 2060, the growth currently enjoyed by developing countries will have petered out, and they will have converged with the stagnation of rich countries. Capitalism (and particularly neoliberalism) is no longer capable of delivering the steady increases in wealth which used to be the only means by which it could be justified.

Since 2008, the financial crisis has pushed neoliberalism towards a more abrupt crisis. The economic crisis quickly became a social crisis, directly linked with emerging civil wars and superpower conflict. Extrapolating current trends over the first half of the twenty first century leads to two plausible trajectories:

- The global elite maintains control; the IMF/WB/WTO retain (weakened) authority over the global economy and the costs of austerity and stagnation are passed on to ordinary people of the developed world.

- The power of elites is broken, and parties of the hard right and hard left take power. The costs of the failure of neoliberalism are imposed not on each countries' own populations, but on neighbouring countries. In some ways reminiscent of the 1930s, globalism falls apart as international institutions lose control and recent conflicts (“drug wars, post-Soviet nationalism, jihadism, uncontrolled migration”2)) flare.

By 2050, climate change, demographic ageing and population growth will make either scenario untenable, and the following decades will be “chaos”.

The purpose of this book is to propose an alternative. Not a plan, but a combination of historical and economic analysis that will illuminate how individuals and the state can nurture the seeds of a new economic order that is already a substantial force worldwide.

Capitalism is a complex and evolving organism that develops new means to neutralise or incorporate emerging challenges. Historically, it has been particularly good at adapting to new technology, but for various reasons, information technology threatens its existence. This technology spontaneously “dissolve[s] markets, destroy[s] ownership and break[s] down the relationship between work and wages. And that is the deep background to the crisis we are living through”3).

The left has been wrong about how capitalism will end. It will not be defeated by governments taking back economic power and reconfiguring production along non-market models. It will be replaced by new forms of economic collaboration that emerge within market economies but which rely on fundamentally different “values, behaviours and norms”4). Postcapitalism is possible because of three features of new technology:

- IT has reduced the need for work and blurred the lines between work and notwork.

- Capitalism can't set prices for information goods because they are not inherently scarce, and the only workaround that capitalism has is to invent new monopolies to create artificial scarcity, which are chronically inefficient.

- Collaborative production is taking off, ignoring markets entirely.

The biggest information product in the world – Wikipedia – is made by 27,000 volunteers, for free, abolishing the encyclopaedia business and depriving the advertising industry of an estimated $3 billion a year.5)

The main conflict of the near future as postcapitalism tries to emerge is between free, abundant goods and “a system of monopolies, banks and governments trying to keep things private, scarce and commercial.”6)

Part I: The crisis and how we got here

Neoliberalism is broken

The way that austerity is discussed is fundamentally dishonest. People are being lead to believe that austerity involves a temporary belt-tightening, whereby we forego wage rises and accept cuts to public services for a decade or less, after which normal service is resumed. In fact, the elite plan is for austerity to be the new normal. As part of austerity, workers rights are to be permanently dismantled.

Simultaneously, since governing institutions have no alternative economic model than neoliberalism, the economic “recovery” that they are constructing contains all of the essential elements of a further crisis. And if a new crisis erupts before the global economy has truly recovered, the same (albeit weak) tools of recovery won't be available a second time. “[T]here are no more bullets left in the clip”.7)

We should listen carefully to the tone in [internal emails between bankers that were published after the crisis] – the irony, the dishonesty, the repeated use of smileys, slang and manic punctuation. It is evidence of systemic self-deception. At the heart of the finance system, which is itself the heart of the neoliberal world, they knew it didn't work.8)

At the same time, technological advancement and rollout has continued through the depression in a way that is unprecedented. The explosive growth technology such as smartphones, solar energy and hybrid cars since 2008 stands in stark contrast to the technological stagnation of the 1930s. This has softened the blow of the depression in human terms, and yet it makes the event more historically significant.

Increasingly, mainstream economists and representatives of governing organisations are predicting that neoliberalism will not recover. This has been termed 'secular stagnation' by Larry Summers, meaning low growth for the foreseeable future. To understand the reasoning behind these predictions, we need to look at four fundamental elements of neoliberalism – factors that created its success but which make its failure inevitable.

Fiat money

Until the 1970s, global trade and finance was based on a system of fixed exchange rates, in which all money was ultimately backed by gold. The US unilaterally abandoned that system in 1971, after which time currencies have been “fiat”. They are not exchangeable for anything, but have value only to the extent that people have faith in the viability and future of the government that backs them (by accepting them as tax payments).

There are many historical examples of fiat currencies collapsing, but they generally involve a loss of confidence in the financial viability of the state. An example of the Texan government in the early 19th century is given. Texas borrowed beyond its means, the value of the Texan dollar collapsed, the population demanded annexation by the United States, and as soon as this became likely the Texan dollar recovered in anticipation that the country's debts would be assumed by the US.

Fiat money is indispensable for neoliberalism, as monetary policy is increasingly used to address every weakening in the economy. In the face of a shock disrupting economic activity, the government prints and injects more money into circulation, lowering interest rates. Low interest rates mean that anybody holding cash cannot get a return from holding government bonds, and so they are forced to invest their savings in more risky alternatives: real estate, shares, gold and commodities. This injection of money into these markets covers up any weaknesses and props up any bubbles.

Until the turn of the century there were (occasional) times when this use of monetary policy was withheld, on the understanding that markets needed to fail to self-correct. One such instance was the Federal Reserve's decision to trigger the dotcom crash of 2001 by raising interest rates to “choke off what [Greenspan] called 'irrational exuberance'”, in recognition of the fact that pumping in more money would only inflate the bubble further, making the crash (when it inevitably came) even larger. However, after 9/11, Enron, Iraq and Afghanistan, rock-bottom confidence in American government and corporations made this sort of economic realism politically non-viable. The Federal Reserve committed to always print money to prevent significant fall in stocks. This changed incentives fundamentally, by announcing that the stock market was now a one-way bet – significant losses would not be tolerated by government.

This was a cause of the crisis, but was also used as the main tool to resolve the crisis. After 2008, $12 trillion (one sixth of global GDP) was printed to revitalise the economy by propping up share and house prices. This also fuelled rapidly rising inequality, because this money is essentially injected into assets: people that own shares, property and commodities see these assets rapidly gain value.

It worked, in that it prevented a depression. But it was the disease being used as a cure for the disease: cheap money being used to fix a crisis caused by cheap money.9)

Financialization

Financialization is made up of four trends introduced as part of neoliberalism from the early 1980s:

- Companies ceased borrowing from banks and sought money on the open market instead.

- Banks turned from productive investment to consumer credit and investment banking.

- Consumers participate more in financial markets through credit cards, overdrafts, mortgages, student loans. Banks have come to earn more from lending money to consumers than profiting from wage labour.

- All simple finance is now resold in more complex, higher-level transactions (derivatives).

Although the relationship is not clear or explained, financialization is “associated with” low wages. Prior to neoliberalism, economic growth require wages to rise so that workers could afford to buy the additional output of a larger economy. But the wages of US production workers have not risen since 1973. Instead, the amount of debt in the American economy has doubled to 3 times GDP. Alongside this, proportion of financial services (broadly defined) in the economy has risen from 15 to 24 per cent, making it larger than manufacturing.

This trend is obviously unsustainable. Once this trend was established in the mortgage industry, a major crash was inevitable. In the last three years before the crash, “'adjustable mortgages', which start cheap and become more expensive as time goes on – came from nowhere to make up 48 per cent of all loans… This market for risky, complex, doomed-to-fail borrowing did not exist until investment banks created it.”10)

This can only be resolved by dismantling financialization, but in the aftermath of the crisis no serious changes have been made. Instead, the system was reassembled and given $12 trillion to get it going again.

There is a strange and contradictory historical precedent. It has been noted that several major empires (the Genoese, the Dutch and the British) turned to financialization as their empires were nearing decline: it has been labelled their “financial autumn”. However, these empires abandoned trade to become lenders, loaning money to the rest of the world. Whereas under neoliberalism, the USA has become the world's borrower. Wage stagnation also bucks this trend: previously declining empires maintained wage growth at home, unlike the US of the last 40 years.

Once every human being can generate a financial profit just by consuming – and the poorest can generate the most – a profound change begins in capitalism's attitude to work.11)

The imbalanced world

Whilst neoliberalism was touted as the answer to the world's economic problems, this was never actually realistic. Neoliberalism's successes were inextricably linked to the fact that large regions of the world, particularly Germany, China, Japan and the oil-exporting countries, not only rejected neoliberalism but made it possible through their complementary role. For neoliberal countries to run current account deficits and borrow beyond their means, non-neoliberal counterparts were needed to export and lend.

These structural imbalances created two risks:

- The West would end up with so much debt that it would collapse. This happened in 2008.

- All the “risk and instability in the world gets pooled into an arrangement between states, over debt and exchange rates, which then collapses. This danger still exists.”12)

All that would be needed to blow the whole thing apart is for one or more country to 'head for the exit', using protectionism, currency manipulation or debt default.

The Republican party currently advocate all three. This is a fundamental flaw of neoliberal economics and neoliberal growth is impossible without it.

The IT revolution

The rapid advance of IT enabled many of the economic changes of neoliberalism, particularly financialization.

However, there is an important economic component of network technologies that sets them apart from other technological advances. Whilst the cost of establishing a network is linear (it costs the same to add each person to the network) the benefits of the network are much greater the bigger the network is. As networks grow, this “network surplus” is created. However, a lot of this value is not market value, it is generated through “non-market interactions” – people communicating with each other outside of a commercial transaction. The recent history of the global IT industry is the story of myriad attempts by capitalism to extract this non-market value, and recurring realisations that this is not necessarily possible.

At the same time, it has had a profound effect in enabling citizens to access information unmediated by elite and state censorship.

The zombie system

A hypothetical recovery of neoliberalism can be imagined, perhaps based roughly on the proposals of “mainstream radical” economists such as Paul Krugman and Joseph Stiglitz. Governments are more restrained in printing money and revive their bond markets, and the implicit guarantee of stock markets and banks is removed. Exchange rates would ultimately return to a global pegged system, with currencies rebalanced to remove the cheap labour advantage of China and India. Imbalances would diminish. Financialization would be reversed, removing political power from banks and reintroducing regulation, increasing reserve ratios and reinstituting the Glass-Steagall Act to separate investment and high street banking.

The problems with this scenario are:

- It will be blocked by elites in all countries who would lose out under this process.

- It would require many sovereign debts to be written off, meaning global creditors would lose vast wealth, breaking an “essential deal” of globalisation. Globalisation would break down and war would be likely.

The OECD, as noted, expects the global economy to stagnate, whilst inequality rises by 40 per cent. By 2060 Sweden will have the level of inequality of the US today. However, in a sense these predictions are wildly optimistic, because the OECD attribute three quarters of the growth over this period to a “rapid rise in productivity due to information technology”.(p28) The report acknowledges that this is “high compared with recent history”. If the network benefits of new technology remain stubbornly resistant to capture by capitalism, the next fifty years could be substantially worse. The OECD's dire predictions also require developed countries to take 130 million migrants to address their ageing population, further diminish labour rights, and fully privatise higher education.

Long waves, short memories

This chapter outlines the main theory of Nikolai Kondratieff,13) a Russian economist working in the early Twentieth Century. His theory has been neglected because it contained undesirable political implications for both the West and the Soviets (who executed him for it), and also because it was incomplete, partially because there was insufficient economic data available at the time. However, several of his key insights were correct, and his work will form the basis of an extended analysis that explains the current economic crisis, and the ways in which capitalism can and cannot adapt to resolve it.

Kondratieff used historical data on industrial capitalism since 1770 to illustrate that long 'waves' exist throughout the history of capitalism. Each wave lasts approximately fifty years. At the beginning of each wave, various new technologies have been invented but not popularised or economically exploited. During the initial “up” phase, lasting about twenty-five years, there is heavy investment in these new technologies, strong growth, infrequent shallow recessions, and conflict between major economic powers over resources and markets. There follows a “down” phase of similar duration, during which investment stagnates, recessions are long and frequent, and capital gets “trapped in the finance system”14)

But Kondratieff was cautious in his conclusions. He believed the duration of the cycles could vary, and emphasised that changing historical conditions meant that no two waves would play out in quite the same way. Further, the work of his colleague, the mathematician Eugen Slutsky suggested that this consistent wave motion could break down temporarily, to be followed by a short or long transition period until a new set of waves emerged.

History has been kind to Kondratieff's analysis. He predicted the Great Depression ten years before it happened. The post-war boom from the late 1940s until the 1973 peak coinciding with the oil crisis and the disruption and stagnation of the 1980s conform to his model as well as any of the previous cycles. And his description of the beginning of a new wave, made up of

- a cluster of new technologies

- new business models

- the addition of new countries to the global trading system, and

- a rise in the quantity of money

closely match the period from the mid-1990s until the financial crash in 2008. Research by Cesare Marchetti in 1986 confirmed these waves in statistics on energy consumption and physical infrastructure. Following previous waves based respectively on canals, rail, paved roads and air networks,

he predicted that a new type of grid should appear around the year 2000. Though writing a mere fourteen years before the millennium he could not guess what it would be. Today we have the answer: the information network.15)

Unlike many of his critics, Kondratieff believed that the causes of the pattern that he had found were economic, not technological; that the pattern of technological invention and rollout were effects rather than causes. He believed that a long wave would begin because so much cheap capital had been accumulated and centralised within the financial system, which could then be used to fund an enormous surge of investment in a revolutionary cluster of new technologies.

Kondratieff's theory has been attacked from the basis of three basic arguments:

- The Marxist critique argues that major changes in capitalism are the result of external shocks, not internal processes.

- Various critics have argued that Kondratieff's data or methods were flawed, and that waves simply don't exist at all or to the extent claimed.

- Contemporary economist Schumpeter argued that the observed waves were caused by the evolution of technology, and the economic phenomena were merely its effects. Various scholars have taken up this argument, to the present. A modern follower of Schumpeter, Carlota Perez, recasts Kondratieff's work in technological terms. For her, each wave begins not with explosive economic expansion, but with the underlying technological advance. This throws out the timeline in an interesting way. It poses the challenge that the fourth wave (1909-71 according to Perez's calculations) was almost seventy years long: her answer is that policy mistakes in the 1930s led to the depression lasting until 1945. Similarly, between 1990 and 2008, there were two separate collapses in the rollout of new technology, where here interpretation leaves room for only one. Again, the explanation is policy mistakes.

Perez's version of wave-theory stresses the response of governments at crisis points, but puts very little emphasis on the struggles between classes or the distribution of wealth. In an almost pure inversion of Kondratieff, the economics are driven by technology, and technology is driven by governments.16)

In addition, Kondratieff hosted a seminar to debate his work a month after publication. During that debate, three main critiques emerged, with varying degrees of validity:

- Economist Dmitry Oparin, argued that a weakness in Kondratieff's methodology had distorted his results. This was answered in further work by Slutsky, who developed important new research in this area, but ultimately sided with Kondratieff in this instance.

- Economist V E Bogdanov found it implausible that the cycle be driven by capital accumulation, and was the first to put forward the argument that the waves were instead driven by technology. He also believed that the non-capitalist world was an important component of the story: that waves must be understood as being a consequence of the interplay between capitalist and non-capitalist societies (in their contemporary wave, the importance of China and the Ottoman Empire). This criticism was valid and this interaction should be included when applying Kondratieff's theory to the present.

- Soviet agrarian economist Miron Nachimson was more concerned with the political implications of the theory. He focused on Kondratieff's insight that capitalism does not merely collapse in the face of crises, but has a long history of mutating to renew itself through new technologies. This contradicted sharply with the Soviet belief that capitalism would imminently destroy itself, foreshadowing Kondratieff's long-term imprisonment and execution.

In summary, then, for Kondratieff's work to be applied to the Twenty-First Century, its weaknesses have to be acknowledged and addressed. Primarily:

- While he correctly understood that the dynamics of capital investment were at the heart of the long wave, his understanding of these dynamics was rather basic.

- He neglected the non-capitalist world in his analysis, when in fact its influence was and is important.

- He did not understand the significance of waves within the “ultimate destiny of capitalism”.17)

Mindful of these gaps, and incorporating Marchetti's related work on physical infrastructure, we can outline a wave history of capitalism to the present:

- 1790-1848: the factory system, steam and canals. Turning point the late 1820s depression. Collapse with the 1848-51 revolutions in Europe, Mexican War and Missouri compromise.

- 1848-mid-1890s: railways, the telegraph, steamers, stable currencies. Peaked in the mid-1870s with financial crises leading to the Long Depression of 1873-96.

- 1890s-1945: electrical engineering, the telephone, scientific management and mass production. Turning point at the end of the First World War, ending with the Great Depression.

- Late 1940s-2008: transistors, synthetics, factory automation, nuclear power and automatic calculation. Peaked with the 1973 oil shock, followed by extended instability but no major depression.

- In the late 1990s, overlapping the previous cycle, the initial elements of the fifth wave appear: the internet, mobile phones and information goods.

But it has stalled. And the reason it has stalled has something to do with neoliberalism and something to do with the technology itself.18)

Was Marx right?

As one of the major historical authorities on crises, Marx enjoyed a bit of a comeback in 2008.

Marxism is both a theory of history and a theory of crisis. As a theory of history it is superb: armed with an understanding of class, power and technology, we can predict the actions of powerful men before they know what they're going to do themselves. But as a theory of crisis, Marxism is flawed… we need to understand his limitations – and the theoretical mess his followers got into as they tried to overcome those limitations.19)

Much of the chapter is devoted to charting the strains of thought that flowed from Marx into the Twentieth Century, most of which took Marx's thought further from the truth because of the political or optimistic necessity of casting capitalism as imminently vulnerable to its one final catastrophe, blinding the left to the complex reality of the system's ability to mutate and adapt. Later, as large national corporations became an obvious stepping-stone to socialism, it was necessary for socialists to ignore the possibility or evidence that capitalism could further mutate into something different. The main analysts who continued in the Marxist tradition failed. Hilferding concluded that

the cyclical crisis was over, Luxemburg [moved] crisis theory to the terrain of collapse, Lenin [assumed] the irreversibility of economic decline. With Varga, we move from rationality to dogma: the least sophisticated of all the crisis theories becomes the unchallengeable doctrine of a merciless state, every communist party in the world becomes its emissary, and every left-wind intellectual for a generation gets taught utter rubbish.20)

Marxist analysis of crises fails in three important ways:

- Capitalism is an 'open' system, i.e. its interaction with the non-capitalist world is important and can't be ignored. This is particularly important in crises, where capitalism often adapts by exploiting new resources or opening new markets.

- Capitalism is a resilient system that is capable of mutating in unpredictable ways in order to resolve crises and create new opportunities for growth and expansion. Most followers of Marx in the Twentieth Century needed to believe that capitalism was imminently vulnerable to its one final catastrophe, either because of political orthodoxy or their own need to believe in a plausible path from their current situation to socialism.

- Systems like capitalism generate 'emergent' phenomena: features that could not have been predicted by constructing a model from its component parts.

For example, the behaviour of an ant colony might be a product of the ant's genetic code, but it has to be studied as behaviour, not genetics.21)

Marx recognised that capitalism has self-destructive tendencies, which operate constantly. Profit is ultimately extracted from labour, by paying labour less than the contribution it makes to the value of the product it produces. But over time, the profit that can be extracted invariably falls. Every established sector or market will experience this decline in returns to capital. This is Marx's “most fundamental law of capitalism”.22)

However, the system also works constantly to counteract this tendency. New markets are created with higher profits, to which investors move their money. Falls in the cost of living (food and consumer goods) can push down the real cost of wages. Cheaper labour can be found abroad, machinery can be made at lower cost, or managers can increase their market share to compensate for lower profit per unit.

On a higher level and over a longer time period, investors can switch from productive investment in order to earn a return on their capital. Under certain conditions the majority of investors may choose to switch to this sort of low-risk, low-return investment, rather than entrepreneurial opportunities.

For Marx, a crisis happens when these counteracting tendencies fail.

That is, when you run out of cheap labour, or new markets fail to appear, on the finance system can no longer safely hold all the capital that risk-averse investors are trying to store there.23)

Marx describes various different kinds of crisis:

- Overproduction: too many goods chasing too little supply.

- Inefficient flow of capital between sectors: investment gets trapped in an area with low profitability and is unable to move to markets with higher returns.

- Failure of counteracting tendencies: as described above.

- Financial crisis: too much credit availability leads to speculation and crime which create a bubble that bursts.

The main function of credit, he wrote, is to develop exploitation 'to the purest and most colossal form of gambling and swindling, and to reduce more and more the number of the few who exploit the social wealth'.24)

The modified Kondratieff wave

There is enough good analysis in Kondratieff and Marx's original work combined to construct a good theory of crisis, and to apply it to the last thirty years. Kondratieff's explanation that there was a need to renew large-scale infrastructure every fifty years was too simplistic. Instead, each wave generates a new set of solutions to the falling rate of profit: a set of business practices, skills and technologies, and the upswing lasts until these become overwhelmed by the tendency of profit to fall as they mature. After the peak, the nature of the decline depends on how successfully countervailing forces can offset falling profits.

Put simply: fifty-year cycles are the long-term rhythm of the profit system.25)

Of particular importance is the role of organised labour during the decline. In each of the first three waves (1830s, 1880s and 90s, 1920s), downward pressure on wages was fiercely resisted, which hastened the onset of the crisis and forced investors to turn to new technologies rather than eke out their existing business models at the expense of their workforce.

The outcome [of class warfare in the downturn] is critical: if the working class resists the attack, the system is forced into a more fundamental mutation, allowing a new paradigm to emerge. But in the fourth wave we found out what happens if the workers do not successfully resist.26)

Transition from fourth to fifth wave

During the fourth (post-war) wave, a substantial part of the world (the Soviet bloc) is closed off: a fifth of global GDP is outside the capitalist system. After 1989 the availability of these resources and markets, and other countries previously under Soviet influence, prolong the wave.

After 1989 [capitalism] experienced a sugar rush: labour, markets, entrepreneurial freedom and new economies of scale.27)

But other factors played into the distortion of the fourth wave, particularly the failure of organised labour, the rise of technology with fundamentally new characteristics, and the “discovery that once an unchallenged superpower exists, it can create money out of nothing for a long time.”28)

The long, disrupted wave

The upswing

The upswing of the fourth wave was unprecedentedly successful. Between 1948 and 1973, Western Europe grew by an average of 4.6 per cent, almost double the rate of the third wave's upswing in 1900-1913. Although many of the sources of this success were common to previous waves, in various ways they were intensified in the fourth:

- New technologies, many developed in wartime, including transistors (i.e. the industrial use of information), synthetic materials, nuclear power, jet engines, integrated circuits and modern management techniques.

- The legacy of the discovery of the effectiveness of wartime state control, which had supported

- a successful and open intellectual property system in which discoveries were exploited in order to profit from production rather than hoarded to extract monopoly rights-based payments; and

- the systematisation and dissemination of management knowledge: the first serious attempts to study and document good management practices and the dissemination of these from one company to the next by management consultancies.

- The feature that was most neglected in contemporary analysis was a conducive and stable financial system, comprising the following (which were all directly or indirectly part of the Bretton Woods agreement):

- Fixed exchange rates: the 1944 Bretton Woods agreement established fixed exchange rates between all world currencies, which ensured that foreign currency transactions were dominated by trade rather than speculation. It was also significant that this system was enforced by a dominant superpower; the credibility of the system increased its value.

- Negative real interest rates. Now described as “financial repression”, in the US between 1948-73, interest rates were on average 1.6 per cent below inflation, so bank savings would lose value over time. This enabled Western countries to recover from high public debts at the end of the war (almost 90 per cent of GDP overall) to about 25 per cent by 1973. It also forced savings into productive investment as the only means of securing a positive return, and controlled inequality. 29)

- National financial systems: strict capital controls prevented international investment, so domestic savings could not seek higher returns abroad but were forced into productive investment at home.

- Highly regulated banks with very high reserve ratios by modern standards (28 per cent in the UK) meant that speculative lending was minimised and prevented bubbles and instability. Bank loans across fourteen Western countries was just one fifth of GDP, the lowest rate since 1870.

Breaking the wave

Considering the inadequacy of the explanations for the dramatic changes in the 1970s, the end of the upturn can best be understood as “a classic phase change on the Kondratieff pattern”, as usual a quarter century into the cycle. The mechanisms are also clear, as we can see many of the drivers of the upswing are exhausted.

The post-war arrangements had effectively locked away instability into two zones of control: relations between currencies and relationships between classes.30)

Both of these broke down in the late 1960s and early 1970s. Firstly, under the Bretton Woods system, the US backed the dollar with gold at a constant price of $35 per ounce. Then, all other countries backed their own currencies with a fixed value in dollars. The problem was that it was possible for countries other than the US to devalue their currencies (more or less unilaterally), thereby giving themselves a competitive advantage against everyone else (and this was a politically benign safety valve where other alternatives were unpalatable). There had been 400 devaluations by 1973. But this option wasn't open to the US, and as other countries caught up with its productivity edge this became a problem. America attempted to use domestic inflation to fight back leading to the inflation crises of the late 1960s. Then the unexpected and extreme failure in Vietnam forced the US to go further, and unilaterally suspend the dollar's peg to gold in 1971.

The relationship between classes was dominated by wages and productivity. During the upswing, rapid productivity increases made high wage increases feasible (and, through consumption, these enabled continued growth). At the same time, full employment ensured that organised labour was steadily gaining power. As in other waves, those productivity increases were not sustained indefinitely. Productivity fell, unions maintained their wage demands, and profits fell by a third by 1973 compared to the wave's peak. Governments responded by pushing up inflation to reduce real wages and by subsidising wages through benefit payments, which grew rapidly, especially in Europe. When Nixon abandoned fixed exchange rates, governments were suddenly able to lower interest rates and increase state spending without limit.

The inevitable stock market crash hit Wall Street and London in January 1973, triggering the collapse of several investment banks. The oil shock of October 1973 was the final straw.31)

The attack on labour

The original concept on which neoliberalism is based is the destruction of working class organisation. In response to the relative power of organised labour in the early phases of the fourth wave, its architects (Pinochet, Thatcher and the “Cold Warriors” who brought Reagan to power) “resolved to smash labour's collective bargaining power, traditions and social cohesion completely.”

Labour had come under attack before – but always from paternalist politicians who had proffered the lesser of two evils: in place of militancy, they'd encouraged a 'good' workforce, defined by moderate socialism, unions run by agents of the state. And they helped build stable, socially conservative communities that could be the breeding ground for ground for soldiers and servants. The general programme of conservatism, and even fascism, had been to promote a different kind of solidarity that served to reinforce the interests of capital. But it was still solidarity.

The neoliberals sought something different: atomization. Because today's generation sees only the outcome of neoliberalism, it is easy to miss the fact that this goal – the destruction of labour's bargaining power – was the essence of the entire project: it was a means to all the other ends. Neoliberalism's guiding principle is not free markets, nor fiscal discipline, nor sound money, nor privatisation and offshoring – not even globalisation. All these things were byproducts or weapons of its main endeavour: to remove organised labour from the equation.32)

During the 1980s, many countries adopted deliberately self-destructive policies in order to deepen the recession, in order to further undermine the working class. High interest rates destroyed many of the large industrial companies in which unions were strongest. In Japan unions were broken by “taking out the ringleaders and beating them physically every day until resistance stopped.”33) But the true success of neoliberalism's attack on labour was at the “moral and cultural level”: union membership drastically declined. “Across the Western world the wage share of GDP fell markedly.”34)

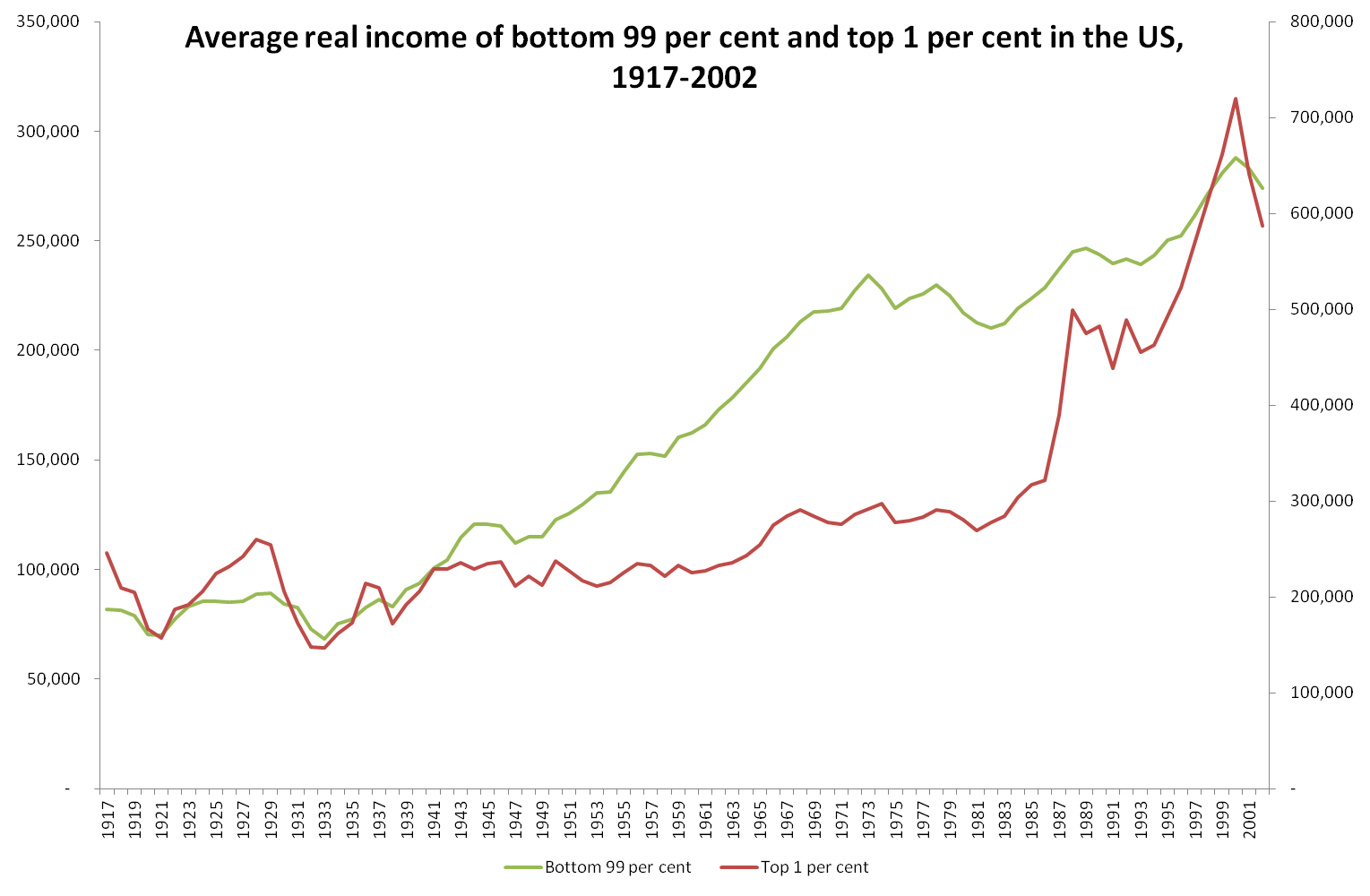

Much of the remainder of the chapter goes through a series of graphical illustrations of the fourth wave. One in particular is important to resolve the common misconception that it is in a ruling class's interests to maintain healthy growth in an economy. This figure illustrates that during the upswing, 99 per cent of society enjoy steady gains in their income, but the top 1 per cent benefited little. During the downswing, this relationship is reversed: 99 per cent of society see their income flatline, but after the assault on organised labour in the early-to-mid 1980s, the income of the highest 1 per cent of earners rockets.

Neoliberalism succeeded in destroying working-class organisation in way that has never happened before, and in the process rebalanced the entire global economy in favour of capital. Kondratieff's theory predicted that we would see downturn and depression, but by breaking labour, neoliberalism managed to convert this into

two exhilarating decades in which an upswing in profits coexisted with social breakdown, military conflict, the return of abject poverty and criminality to communities in the West – and spectacular riches for the 1 per cent.36)

Part II: A theory of postcapitalism

The prophets of postcapitalism

This chapter outlines a list of contributions from authors that have played with “postcapitalist ideas”, which have been variously labelled “the knowledge economy”, “the information society”, “info-capitalism” and “cognitive capitalism”.

In general these authors offer isolated insights. A common weakness is to lazily declare that a new mode of production has arrived, and the world economy has already transitioned to it. Perhaps only a British journalist could write that

This is a technique common in European speculative thought: to invent a category and apply it to everything, thus reclassifying existing things as sub-categories of your new idea. It saves you the trouble of analysing complex and contradictory realities.37)

They come from a variety of disciplines: law, economics, technology and history, at minimum, and a true understanding of how society is changing and could change further needs to recognise how these trends fit together, and importantly the synergies and tensions between nascent developments and existing neoliberal production. Some come from very mainstream neoliberal thinkers (who tend to see this development as a benign triumph of neoliberalism), others from the left. In their more exalted moments, they see this new form of info-capitalism as capitalism's “third phase”, after mercantilist capitalism and industrial capitalism.

We will try to keep an account of these origins to a minimum, because the important content here is how they are synthesised by Mason into a comprehensive theory.

Peter Drucker was a management guru who wrote The Post-Capitalist Society in 1993. He posed two main questions, the first being, “How do we improve the productivity of knowledge?”38). Connecting knowledge from different spheres to an unprecedented degree through networks vastly increases the potential for knowledge production. Secondly, he asked “Who is the social archetype of postcapitalism?”39) His answer is “the universal educated person”: somebody with a basic general education who can take advantage of easily accessible knowledge by applying it.

Paul Romer is a mainstream American macro-economist who published the paper Endogenous Technological Change in 1990. This was a dry academic attempt to place innovation into the economic theory of growth, assuming that technological change was a driver of economic growth and therefore looking at how an economy can drive faster technological change. He discovered that “instructions for working with raw materials are inherently different from other economic goods”, so that an economy based on information products will be entirely different from one based on physical goods.

Most importantly, information goods make perfect competition impossible. They push industries towards imperfect competition. In order to run a large business based on information goods, it is necessary to establish an elaborate monopoly. For Apple to sell music, in requires the aggressive use of copyright law, but also an expensive physical network of technologies: “the Mac, iTunes, the iPod, the iCloud, the iPhone and the iPad – to make it easier for us to obey the law than break it.” This is because the traditional market mechanism of supply and demand is irrelevant when supply is effectively infinite at zero marginal cost. Although Romer is a respected and successful professor, the economics profession greeted this paper with “hostility and indifference”.40)

The Free Software Foundation and its founder Richard Stallman have created a community based on voluntary contribution of work in a non-hierarchical network that generates products that are freely distributed. It began with the GNU project to replicate the UNIX operating system with a free alternative. This project incorporated Linux, and intellectually spawned allied projects such as Wikipedia and Firefox. The two “most important document[s] in the history of digital economics”41) were, secondly, an open letter by Bill Gates to communities of computer enthusiasts that copied software illegally:

Most of you steal your software. [You believe] hardware must be paid for but software is something to share. Who cares if the people who worked on it get paid.42)

and, firstly, Stallman's GNU Manifesto:

If anything deserves a reward, it is social contribution. Creativity can be a social contribution, but only in so far as society is free to use the results. Extracting money from users of a program by restricting their use of it is destructive because the restrictions reduce the amount and the ways that the program can be used. This reduces the amount of wealth that humanity derives from the program.43)

Next, US journalist Kevin Kelly wrote for Wired and a book New Rules for the New Economy in the late 1990s. His insight was that the revolution of cheap computation was already over. The changes it had made to society were already apparent. The much bigger revolution to come was based on the interconnection of computers, the “Internet of Things” as it has come to be known.

I prefer the term network economy, because information isn't enough to explain the discontinuities we see. We have been awash in a steadily increasing tide of information for the past century… but only recently has a total reconfiguration of information itself shifted the whole economy.44)

He accepted the implication of Romer's work, that information technology would endlessly make products cheaper as the marginal cost of production approached zero. But he believed that this would be counterbalanced by inexhaustible supply, as “human imagination” endlessly invented new products and combinations of products for which the cost of production was still (temporarily) finite. Neoliberalism would survive, and those that understood the new technology would flourish. Then came the dotcom crash.

Yochai Benkler, one of the architects of Creative Commons licences (a legal framework which protects sharing various kinds of content) wrote The Wealth of Networks in 2006. Cheap computing power plus networks enable people to produce valuable products through non-commercial processes of interaction: “as human beings and as social beings, rather than as market actors through the price system.” Wikipedia is the most successful archetype, and has both out-competed its capitalist competition, and made the idea of a new encyclopaedia created through capitalist production processes unthinkable.

Economists like to demonstrate the archaic nature of command planning with mind-games like 'imagine the Soviet Union tried to create Starbucks'. Now, here's a more intriguing game: imagine if Amazon, Toyota or Boeing tried to create Wikipedia.45)

At the end of the Nineteenth Century, economists developed their understanding of “externalities”: beneficial or detrimental side-effects of market transactions. The information economy drastically escalated their importance, suddenly externalities could dominate the market transaction entirely. Society's first response to this was to create “public goods” like science: society pays for the production of science for the good of everyone, because the amount of benefit that can be captured by privately commissioning science is a tiny fraction of its value if it is released for the benefit of everyone. But Kenneth Arrow, a mainstream economist in 1962 argued that under capitalism, the purpose of creating information is (or should be) to capture private benefits by enforcing intellectual property rights.

Precisely to the extent that it is successful there is an under-utilisation of information.46)

In other words, the success of your exploitation of your intellectual property rights can be measured by all the things you manage to prevent society from doing with the information you created.

If we restate Arrow's observation in a different way, its revolutionary implications are obvious: if a free-market economy with intellectual property leads to the underutilisation of information, then an economy based on the full utilisation of information cannot have a free market or absolute intellectual property rights.47)

Although closely associated with a radically different type of transition from capitalism, Karl Marx provided some of the greatest insights into postcapitalism in a notebook that remained unpublished until the late 1960s and was only translated into English in 1973. In the Fragment on Machines Marx explores the idea of machines becoming so sophisticated that labour ceases to be a significant part of the production process, but rather the role of labour is to design, repair and oversee mechanical production. Here, he concludes, the most important factor of production becomes the “general intellect” – the shared body of knowledge from which the design of the machines is derived. And capitalism is forced to develop the intellect of the worker and will tend to reduce working hours.

It is impossible to properly value inputs when they come in the form of social knowledge. Knowledge-driven production tends towards the unlimited creation of wealth, independent of the labour expended…

[K]knowledge-based capitalism creates a contradiction… [creating] 'the material conditions to blow [capitalism's] foundation sky-high.'48)

Postcapitalism: a hypothesis

Since the 1990s, information technology has undermined capitalist property relations thus:

- the price mechanism for digital goods breaks down, as the marginal cost of production hits zero

- physical goods gain a high information component, forcing them into a dynamic in which their marginal cost is constantly approaching zero

- the value of physical goods may lie more in social relations than in physical attributes (i.e. the brand premium))

- financialization extracts more and more profit from consumers through interest charges on their consumption, in addition to traditional capitalist exploitation of workers

- consumers are also exploited in lesser ways through the extraction of brand value and the capture of externalities by firms (the data that is collected from your use of the internet is packaged, sold, and then used to make more money out of you))

As information constantly corrodes value, firms have three possible responses:

- establish a monopoly, generate IP and sue everyone,

- constantly create new products and make money out of them in the brief period before they become valueless, or

- capture externalities by collecting consumer data and exploiting it.

However, parallel to firms' response, people are now producing value through peer-production with zero or negligible “market” component. In some areas this is wildly successful and destroys all capitalist competition within a decade.

In response, capitalism is beginning to reshape itself as a defence mechanism against peer-production, through info-monopolies, through allowing the wage relationship to weaken and through the irrational pursuit of high-carbon business models.49)

There is a fundamental contradiction between the “social” and “technological” dimensions if this change.

Technologically, we are headed for zero-price goods, unmeasurable work, an exponential takeoff in productivity and the extensive automation of physical processes. Socially, we are trapped in a world of monopolies, inefficiency, the ruins of a finance-dominated free market and a proliferation of 'bullshit jobs'.

Today, the main contradiction in modern capitalism is between the possibility of free, abundant socially produced goods, and a system of monopolies, banks and governments struggling to maintain control over power and information. That is, everything is pervaded by a fight between network and hierarchy.50)

It is uncertain how this will play out. Capitalism may maintain control and absorb these new technologies into familiar hierarchical power structures, and either capture or neutralise the potential of networks. Or the network undermines both the functioning and the credibility of markets and there is a significant shift in societal power and the dominant mode of production. Given the amount of power stacked behind existing hierarchies, if the transition to postcapitalism happens then it will be the result of an intense fight with those who are pushing for change.

We'll know it's happened if a large number of goods become cheap or free, but people go on producing them irrespective of market forces. We'll know it's underway once the blurred relationship between work and leisure, between hours and wages, becomes institutionalised.51)

Towards the free machine

This chapter outlines two competing theories of how the price of goods come to be set. Mainstream economics' understanding is based on marginal utility, which is able to make accurate predictions about the movement of prices in established markets. However, it is a static theory: it does not encompass crises, and is unable to explain historical changes.

The labour theory of value is perhaps a “higher level” theory, that predicts historical dynamics and explains why capitalism tends towards crisis. It is less easy to use to make quantitative predictions about individual markets, but the main reasons that it fell out of favour in the nineteenth century were political. It suggests that all value is created by workers, and the implications of that for the fair distribution of wealth were uncomfortable for elites, as much in the nineteenth century as today. As a result, although there are many distinguished scholars who believe the labour theory of value and teach it as fact, there are very few that are permitted to teach in economics departments.52)

The labour theory of value

The basic idea that the ultimate source of value is labour is as old as economic analysis. It was first proposed by Adam Smith and taken up by David Ricardo, but its most complete form is in the work of Karl Marx.

Under this theory, the entire value of products can be traced back to the hours of labour that went into their creation. Although the price paid for a good in any given transaction can be influenced by many other things (which Smith lumped together as “haggling”), in the long term the price must settle to the sum total of all socially necessary work required to create it. However, this labour value can be divided into two:

- finished labour is labour that is “encapsulated” in machinery, energy and raw materials. As with any other product, these are viewed as the product of labour, so the value of a machine is the sum of all the labour needed to create that machine. Importantly, the amount of finished labour that goes into a new product created with the help of a machine is equal to the labour value of that machine divided by its lifespan. So a machine that cost 5,000 hours of labour to produce and lasts 10,000 hours before it must be replaced costs 30 minutes of labour value to use for an hour. If that machine can be used to make 3 goods in an hour, then each unit requires 10 minutes of “finished labour” value.

- living labour is more familiar: it's the labour that is directly used to create the product. If a good takes an hour to make, it embodies one hour of “living labour” value.

Three further questions establish the framework:53)

- What determines the value of labour? The answer is the same as for other goods: the labour value. A worker needs food, shelter, transport, clothing, heating, leisure, etc: the combined labour value of all of these goods determines the labour value of labour.

- Where does profit come from? Profit comes only from the difference between the labour value of labour (which must be paid to the worker) and the number of hours of labour that that worker works in exchange. Perhaps it costs the equivalent of four hours of labour for a worker to pay for all the things necessary to come to work for a day: then four hours labour will be the daily wage. But if the firm can extract 8 or 10 or 12 hours of labour from the worker that day, then it has made a profit. Profit is only derived from labour (not from capital, land, rent etc).

- Why would a worker accept less than the true value of his labour? Because “the labour market is never free.”54)

At the dawn of capitalism, average working days of fourteen hours or more were imposed – not just on adults but on children as young as eight. A rigid system of timekeeping was implemented: rationed toilet time, fines for lateness, product defects or talking, enforced start times; and immovable deadlines. Wherever we see the factory system created afresh – whether in Lancashire in the 1790s or Bangladesh in the last twenty years – we see these rules enforced.

Even in advanced countries the labour market is built overtly on coercion. Just listen to any politician make a speech about welfare: cutting unemployment and disability benefits is designed to force people to take jobs at wages they can't live on. In no other aspect of the market does the government coerce us to take part; nobody says 'You must go ice skating or society will collapse.'55)

Marginal utility

The theory used by mainstream economics focuses not on the workplace but on the market. It is based on the idea that a consumer will pay a price equal to the last unit of a good that they are willing to buy. If I can buy a chocolate bar for $1, I will keep buying chocolate bars until the last chocolate bar is less use to me than the dollar I would have to pay for it. This insight enables analysis of markets for scarce goods that leads to useful predictions about how they will behave. But it predicts stability: markets tend towards equilibrium. This is an accurate prediction of observed fact the vast majority of the time (and its predictions can be precise). But it cannot explain how crises originate, so mainstream economics can only conclude that it comes from “somewhere else”: something outside their model.

Labour value and information

The labour theory of value predicts historical dynamics. Firms seek profits, and one way to earn profits is to improve productivity. That means reducing the amount of labour required to make your product. Then you can capture the difference between the price you are still charging and the reduced amount that you are paying to your workers, until other companies have copied you and the market price of your product has fallen.

The problem is that this improvement in productivity has reduced the amount of labour embodied by your product. Now a higher proportion of the cost of production comes from “finished labour” (machinery, energy, raw materials) and a smaller proportion from labour. But labour is your only source of profit: so in the long-term stable state, profit for everyone in the industry has declined. And this will keep happening.

To counteract this, you will need to find new products or markets where the labour content of production is higher, so that you have more to exploit. This could mean new physical markets (oversees) or the commercialisation of previously non-market areas of life (like the advent of paid entertainment such as the cinema for the working class in the early twentieth century). If these new sources of revitalised profit do not materialise, then capitalism is heading for a crisis.

Under the labour theory of value, machinery erodes, and it is the value of that erosion that makes up the “finished labour” component of a product's value. Because of this conception of the cost of capital, a machine that does not erode – that never needs to be replaced – is effectively free. 56) As all products progressively incorporate information as a larger share of their value, we will see much more of our capital approach this ideal.

An analysis of what happens when capital is free reveals that it reduces the value (and price) of labour. Recall that the value of labour is determined by the cost of all the labour that is required to sustain labour. Many of these things are capital costs (such as housing). Effectively free capital means that workers need to spend less to live, and iteratively reduces the labour value of labour. Over time, energy and raw materials increasingly tend to dominate the cost of all goods.

Two outcomes

To survive and mutate into info-capitalism, our economy needs to use the standard countermeasures to address falling profits in the face of free information and free machinery: new markets or new consumer needs. It would have to:

- use monopoly pricing

- maximise the capture of externalities by corporations, by scrutinising every interaction between people and using that data for profit

- maintain high prices for energy and raw materials by hoarding

- create new service jobs by pushing market transactions into previously unmonetised areas: “creating new forms of person-to-person micro-services, paid for using micro-payments”

- find work for the millions of people whose jobs are about to be automated, starting with the 27 per cent of American workers employed in 'office and admin support' or 'sales'

The elements of this are already in place:

Apple is the classic price monopolist, Amazon's business model the classic strategy for capturing externalities; commodity speculation the classic driver of energy and raw material costs above their value; while the rise of personal micro-services – dog minding, nail salons, personal concierges and the like – show capitalism commercialising activities we used to provide through friendship or informality.57)

However, there are problems:

- The normal resolution to the crisis is blocked. Information changes production permanently because it will give all new technologies “the zero-price dynamic”.58) There cannot be a 25-year upswing in the face of this.

- The necessary scale of workforce redistribution to deal with automation is untenable. A 2013 study by the Oxford Martin School argued that 47 per cent of all US jobs can be automated.

- This redistribution would require the service sector to explode, amounting to a “mass commercialisation of ordinary human life.”59)

You could pay wages for housework, turn all sexual relationships into paid work, mums with their toddlers in the park could charge each other a penny each time they took turns to push the swings. But it would be an economy in revolt against technological progress.

Early capitalism, when it forced people into factories, had to turn large parts of the non-market lifestyle into a serious crime: if you lost your job you were arrested as a vagrant; if you poached game, as your ancestors had always done, it became a hanging offence. The equivalent today would be not just to push commercialism into the deep pores of everyday life, but to make resisting it a crime. You would have to treat people kissing each other for free the way they treated poachers in the nineteenth century.60)

- Property rights would have to be violently maintained, and yet the technology to make them untenable in their current form is already ubiquitous.

An economy based on information, with its tendency to zero-cost products and weak property rights, cannot be a capitalist economy.

The usefulness of the labour-theory is that it accounts for this: it allows us to use the same metric for market and non-market production in a way that the OECD's economists could not.61)

Beautiful troublemakers

This chapter is a history of the proletariat since the early days of capitalism. It charts the evolution of

- workplaces and the nature of their work,

- relations between different working class groups (especially skilled/semi-skilled, men, women and children),

- the nature of their conflicts with bosses and governments,

- changes in their material conditions, caused both by unionist victories and defeats, and the influence of Kondratieff waves, and

- their aspirations, especially the dichotomy between revolutionary socialism and establishing more control and better conditions over their lives and work.

Another feature of the earlier phases is to point out mistakes in the writing of Marx, Engels and Lenin. In particular, in contrast to Marx's powerful analysis of capitalism, his understanding of the working class was weak and full of errors.

1771-1848

During the first phase, workplaces tended to centre around skilled, adult male guilds, with women and children providing unskilled labour. Marx characterised them as alienated by their lack of “craft, skill, religion and family life”62) and thereby apt to agitate for aims that were then popular in the German middle-class: socialist revolution and the abolition of private property. But instead they overcame the alienation shock of migration to factory work by constructing a culture of “learning, humanity and self-help”, and fought capital for more modest objectives, above all control of their work.

Capital responded by targeting the most skilled workers and trying to use automation to break their power. This was another source of Marx's confusion. He saw this process of automation as inevitably leading to further alienation and lowering wages, but generally speaking it failed. Automation came, but while it reduced the labour content of production, it rarely reduced the need to employ highly skilled workers who retained the ability to down tools.

Engels' anthropology of the English working class in 1842 is detailed, complex and specific. The Marxist theory of the proletariat is not: it reduces an entire class to a philosophical category.63)

1848-98

After mid-century instability, the upswing of the second wave brought strong economic growth. This period was characterised by strong trade unions of skilled workers across the West, albeit in larger workplaces with less guild insularity than before. Employers found it easier to give in to their demands than to resist. Even after the peak, the unions retained their strength and were largely able to resist attacks on their wages and workplace autonomy, although their aims and demands did not extend beyond these basic objectives. Marx saw the situation in England as an anomaly that was only possible due to colonial exploitation abroad, and refused to see that the pattern was in fact similar in other countries.

It was a near-total misreading of the situation. Skill, passivity and political moderation were pervasive all across the workforce of the developed world during the second half of the nineteenth century.64)

1898-1948

In the third wave, a generation of entrepreneurs including Frederick Winslow Taylor and Henry Ford believed that the way to break the power of the skilled unions was not so much automation as to break each skilled task down into simple units that could be taught quickly and easily. The resulting work was much more dull and repetitive than before, and

Taylor wrote that the type of man suited to such work was 'so stupid and so phlegmatic that he more nearly resembles in his mental make-up the ox than any other type'.65)

In the process, there was a great upskilling of a large number of workers from unskilled to semi-skilled. Over time these semi-skilled workers became “educated, radicalised and political”66) and union membership exploded.

Alongside this, Vladimir Lenin was deciding that working people were not capable of fulfilling the destiny that Marx had assigned to them, and would need to be led by an intellectual vanguard. He also had to deal with the unfortunate surge in patriotism across the developed world that came along with the war. He blamed the 'labour aristocracy' – the skilled workers who were the “source of patriotism and moderation polluting the labour movement”.67) Lenin doesn't discuss the origins of skilled labour's privileges, it is almost as if he assumes that capitalists granted those privileges rather than doing everything they could to destroy skilled labour.

By now, Lenin was a long way from both Marx and Engels. For Marx, the working class is capable of becoming communist spontaneously; for Lenin it is not. For Marx, skill is destined to disappear through automation; for Lenin, skilled privilege at home is the permanent result of colonialism abroad.68)

Unions were important in disrupting and ending the First World War. This began with strikes in Berlin, Glasgow and Petrograd in 1916 and '17, and a widespread mutiny in the French army in 1917. Workplace control had been established by factory committees in Russia that later had to be dismantled in order for Lenin to consolidate power. Then the opposition of German unions to the war ultimately led to its end, with revolution narrowly avoided after a mainstream socialist party joined and co-opted the rebellion.69)

Within forty-eight hours of the mutiny [of German naval workers], they had forced an armistice, the abdication of the Kaiser and the inauguration of a republic.70)

The interwar period saw unions take a more radical position, vacillating between revolution and reform. Communism may not have been their instinctive goal, as Lenin had said, but their ambitions certainly extended beyond pure trade-unionism.

Their spontaneous ideology was about control, social solidarity, self-education and the creation of a parallel world.71)

However, the Wall Street crash marked the peak of the third wave, and the conflict between labour and capital rapidly intensified.

The stage was set for the decisive event of the 200-year history of organised labour: the destruction of the German workers' movement by fascism. Nazism was German capitalism's final solution to the power of organised labour.72)

As the 1930s wore on, the conflict turned violent across Europe: in a civil war in Austria in 1934, in Spain from 1936, and in Greece under the Mataxis dictatorship – and the unions lost.

The workers who fought fascism were the most class-conscious, self-sacrificing and highly educated generation in the entire 200-year history of the proletariat.73)

As well as the physical destruction of workers, whether in concentration camps or on the battlefield, the extreme left failed to understand what was happening. Trotsky maintained the traditional line of refusing to participate in wars between imperialist powers, utterly failing to understand that “by May 1940 the war was a bigger fact than class struggle”.74) What followed was an uneasy alliance between organised labour – cognisant that their survival required the physical destruction of fascism – and the Allied powers, who were more than happy to halt their advance to allow the Wehrmacht to deal with any potentially troublingly militant working class rebellion.

1948-89

At the end of the war, elites genuinely feared revolution in a wide range of countries, and profound accommodations were made to labour in the form of welfare states and legal protection of union activity. Welfare states were even “imposed” on defeated enemies “as a punishment for their elites and as an obstacle to their re-emergence as fascist powers.”75) The global economy took off and output and wages rose rapidly. The success of Keynesian demand management created a new consensus in which government was expected to guarantee full employment.

When the peak of the wave came, the Keynesian consensus broke down rapidly but not in a single event. By 1971 the upswing was over, but counterintuitively the breakdown of fixed exchange rates gave governments a brief breathing space and the power to make everything worse by hiking “the social wage”76) to 13.5 per cent of GDP across the OECD. The economy would inevitably turn a corner into the decline of the wave, but workers held too much power to accept the consequences.

The standardised production process of the post-war era… ended up creating a workforce it could not control. The mere fact that the work-to-rule actions became the most effective form of sabotage tells the real story. It was the workers who really ran the production process. Any proposal to solve macro-economic problems without their consent was pointless.77)

The elite response was a group of politicians who were prepared to destroy the economy in order to break union power, and the second oil shock in 1979 offered them the opportunity to launch their project. Labour's greatest analytical mistake was failing to foresee the

part of the workforce [that was] prepared to side with conservative politicians… many skilled British workers, tired of the chaos, swung to the Conservatives in 1979 to give Thatcher ten years in office. Outright working-class conservatism had never gone away: what it always wants is order and prosperity, and by 1979 it could no longer see these things being delivered by the Keynesian model.78)

Part III: The transition to postcapitalism

On transitions

This chapter looks at two historical transitions between economic models in order to draw out lessons for the forthcoming transition to postcapitalism. However, it is concluded that there is much more to learn from the second (feudalism to capitalism) than from the first (the Russian system of quasi-feudalism and early capitalism to Soviet state planning).

Soviet transition

The transition to Soviet planning went wrong in phases:

- 1918-21: under civil war conditions, industry and finance were nationalised, production was directed by commissars and food was requisitioned from peasants. Output fell by 80 per cent.

- From March 1921: the market for food was restored, with peasants paid for their produce. Better off peasants benefited, and the price of food throttled industrial development. Government bureaucracy was solidified.

- A dispute emerged:

- Trotsky and the working class pushed for more democracy, less speculation and industrialisation through central planning

- Bukharin preferred greater restoration of markets, delayed industrialisation and support for a peasantry enriching itself, while

- Stalin merely defended the interests of the established bureaucracy.

This was resolved when Stalin expelled rivals and then adopted parts Trotsky's proposal in an extreme and violent form, destroying the wealthier peasantry through enforced collectivisation, killing 8 million people in 3 years in order to kickstart industrial development which aimed to catch up with the West in 10 years.

The USSR did not catch up with the West in ten years. But by 1977 its GDP per head was 57 per cent of the USA's – which put it on a par with Italy. From 1928 until the early 1980s, the average growth in the USSR, according to a CIA-commissioned survey, was 4.2 per cent. 'This clearly qualified as a sustained growth record,' concluded analysts at the RAND corporation.79)

However, the RAND study80) concluded that only a quarter of this growth had come from productivity increases, the rest coming from increased inputs. For this reason, this growth was not sustainable – exponential growth is not typically considered possible simply by amassing ever greater quantities of capital in this way (according to mainstream economic theory).

At this point the book contains an incongruous attack on state planning, which is odd for two reasons. First, it seems unlikely that many readers need convincing that in 2015 a new system of state planning will rescue the global economy. Second, the entire thing is a straw man, attacking laughably weak examples of state planning (namely pre-war Soviet attempts and an academic political science project run by a couple of guys in Europe), pretending that a single failed example proves all attempts impossible and studiously avoiding credible alternatives.81)

Mason concludes that the main lesson to learn from the Soviet transition is that “a transition phase generates its own dynamics; it is never just the fading of one system and the rise of another.”82)

From feudalism to capitalism

The transition from feudalism to capitalism was, of course, extremely slow. But the most important observation is that this wasn't merely a transition from one sort of economy to another – that is a modern perspective that is natural only to us because our current society is dominated by market economics. The transition was really about the market becoming important, or even the market coming to exist for the first time.

Feudalism was a system based on obligation: peasants were obliged to hand part of their produce to the landowner and do military service for him; he in turn was obliged to provide the king with taxes, and supply an army on demand.83)

And here's where the mode of production concept gets challenging: the changes are so huge that we are never comparing like with like. So when it comes to the economic system that replaces capitalism, we should not expect it to be based on something as purely economic as the market, nor on something as clearly coercive as feudal power.84)

Feudalism ended for four reasons:

- In the early 1300s the system was heading for a crises as productivity increases petered out and the English monarch defaulted on his debts in 1345. Then came an external shock: the Black Plague (1347 onwards) wiped out a quarter of the population, leading to a shortage of labour, surging wages and violent economic struggle, whilst production switched from food to wool and mercenaries became much more important in warfare.

- The expansion of banking created an “alternative network of power and secrecy”85), an early capitalist institution that began influencing power centres.

- The conquest of the Americas brought in an unimaginable surge of wealth, which was channelled to monarchs rather than the lords that had traditionally overseen wealth creation.

- The printing press (1450) created more books in its first fifty years than had been produced since Roman times.

If the medieval cathedral was full of meaning – an encyclopaedia in stone – printing destroyed the need for it. Printing transformed the way human beings think…

If we accept the four-factor account given above, the dissolution of feudalism is nor primarily a technology story. It is a complex interplay between failing economics and outside shocks. These new technologies would have been useless without a new way of thinking and the external disruptions that allowed new behaviours to flourish.86)

Many of the external shocks that will shape the transition from capitalism are already well known: “energy depletion, climate change, ageing populations and migration”.87) Whereas twentieth century leftists have tended to believe that a gradual transition beyond capitalism was not possible whilst the alternative was central planning, this has turned out not to be true. Once dreams of success began to fade, the left focused simply on clinging to privileges previously won, such as free healthcare and union rights.

Today we have the relearn to do positive things: to build alternatives within the system; to use governmental power in a radical and disruptive way; and to focus all our actions towards the transition path – not the piecemeal defence of random elements of the old system.88)

The rational case for panic

This chapter describes two imminent shocks to the global economy that will determine the context in which neoliberalism will end. Each will make the transition more difficult and prone to social and economic breakdown. An attempt to transition to a postcapitalist economy will have to address both seriously, which in turn will determine which strategies are feasible.

Climate change

I've avoided 'building in' the climate crisis until now. I wanted to show how the clash between info-tech and market structures is, on its own, driving us towards an important turning point. Even if the ecosphere was in a steady state, our technology would still be pushing us beyond capitalism.89)